Since we first published our analysis of India's economic recovery from COVID back in September the leading indicators have shown continuous improvement. As we enter India's all-important festival season we take an updated look at the data and find renewed grounds for optimism as well as some cautionary signals to help guide decision-making in the months ahead.

Snapshot of India's economic recovery

India's economy is recovering from the impacts of the COVID-19 pandemic, with GDP expected to grow by 7.5% in 2021. However, the country is facing challenges such as supply chain disruptions and rising inflation. It is important for businesses to stay informed about the economic indicators in India and to prepare for potential challenges as the recovery continues.

- Charts |

- 12 November, 2020

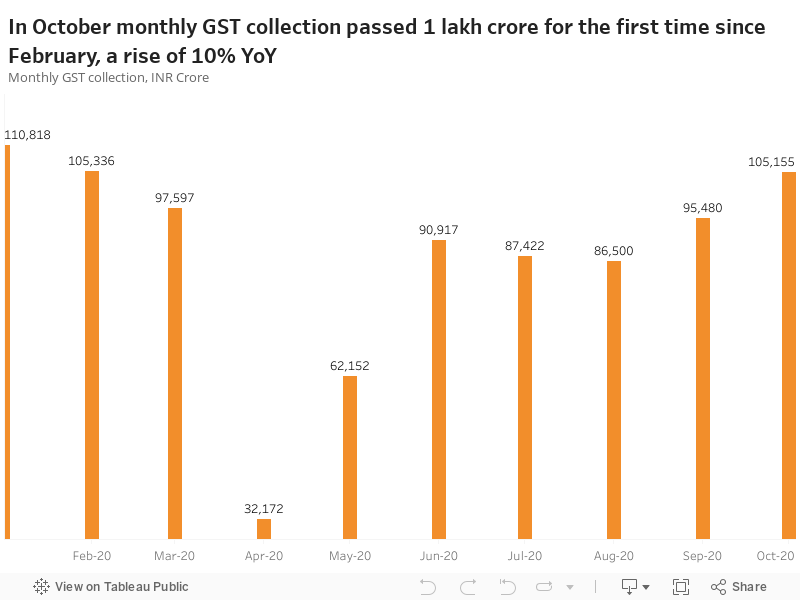

GST collections continue upward trend

In a strong signal of demand recovery, GST collections resumed their upward trend in September and October after stagnating over the summer months. In October total collections surpassed 1 lakh crore for the first time since February, a figure that is 10% higher than the same month last year.

Manufacturing and service sectors see expansion

Thanks to a recovery in demand and a continued relaxation in COVID-19 restrictions October and November saw an expansion in both India's manufacturing and services sectors for the first time since the crisis began. The Purchasing Managers Index (PMI) continued the upward trend of recent months as production rose at its fastest pace since late 2007.

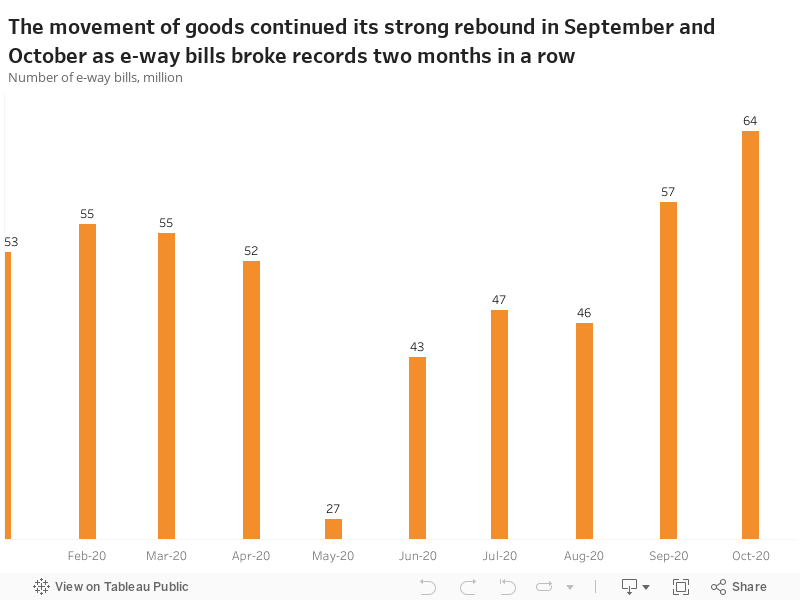

E-way bills pick up speed

In a further sign of accelerating economic recovery, the number of e-way bills hit an all-time high of 5.74 crore in September and broke the record again in October to reach 6.42 crore.

Fuel and electricity demand power ahead

In a strong signal of recovering industrial and consumer activity, monthly electricity consumption in September rose above last year's levels for the first time since the onset of the coronavirus crisis. This helped moderate the drop in H1 demand to -7.9%. This positive trend continued in October with power demand 12.1% higher than last year.

These trends were also reflected in petrol consumption which passed 2019 levels in October for the first time since the pandemic while diesel demand continued to move upward although remaining slightly below last year. The growth in fuel demand reflects the increase in movements of private and commercial vehicles as consumers spent more time out of their homes and the demand for goods accelerated.

COVID cases fall back from peak

Average daily new infections have fallen by around 50% since their peak in late September bringing hope that the worst of the virus may be behind us. However, in the most recent week, the fall has stopped reminding us of the need for constant vigilance.

India is on the move again

As we enter the festival and wedding season in India previously homebound consumers are on the move again. Google mobility data shows that Indians spent increasing time at stores, parks, and transit stations in October while spending less time at home. Visits to grocery and pharmacy stores are now 10% above the pre-COVID levels.

Consumers future outlook improves

Although Indian consumers' confidence about the current situation remains at record lows their future outlook has improved rising from a low of 86 in April to 106 in September. As consumers become increasingly confident about the economy's longer-term prospects they are more likely to bring forward spending decisions that will feed through into higher economic growth.

India's economic outlook lags

Despite the signs of improvement in the last few months India was the only major economy to receive a downgrade from the International Monetary Fund (IMF) in their updated World Economic Outlook for October. The IMF projected India's GDP growth for 2020 at -10.3% which was a downward revision from -4.5% in June. This compared with an upward revision for China from +1% to +1.9% and for the US from -8% to -4.3%.

Export growth surges in September but slows in October

After exports surged in September above 2019 levels there was a significant fallback in October due to a combination of lack of container availability as well as domestic disruptions caused by farmer agitations in various parts of the country - highlighting how both COVID and non-COVID risks could threaten recovery.

Inflation continues to tick up

After easing during the first quarter following the demand shock caused by lockdown inflation in India is on the rise again - increasing from 6.7% in August to 7.3% in September and 7.6% in October. A continuation of this trend could threaten the country's economic recovery by further eroding consumers' spending power.

Europe and the US succumb to a second wave

As we enter winter in the northern hemisphere both Europe and North America are firmly in the grip of a second wave of COVID-19 infections. Major economies like the US, UK, Germany, France, and Italy have all reached record highs and as a result, many countries have re-implemented restrictions. This could have a dampening effect on global growth in Q3 and also flashes a warning signal to India about the risks of a potential resurgence of the virus.

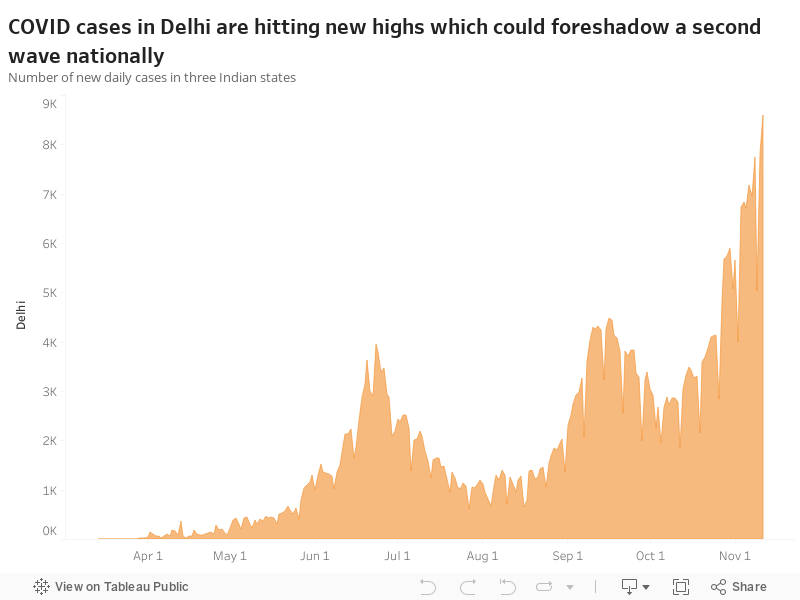

COVID resurgence in Delhi could foreshadow a second wave

While cases nationwide have fallen, a rise in new infections in Delhi since late October could foreshadow a second wave across the country. Increasing movement of people during the current festive season along with lockdown fatigue is a significant cause for concern.

Corporate stresses ease but recovery is painfully slow

The first quarter of FY21 saw record rating downgrades of Indian corporates as the COVID-19 shock rippled across industries. While the ratio of upgrades to downgrades marginally improved in the second quarter the rate of recovery remains painfully slow with major implications for the private sector's investment capacity going forward. However, several sectors saw standout improvement notably healthcare, financials, pharmaceuticals, fertilisers, and sugar.

Related Insights

- Article |

- 19 October, 2020

- Charts |

- 10 September, 2020

- Article |

- 01 October, 2020