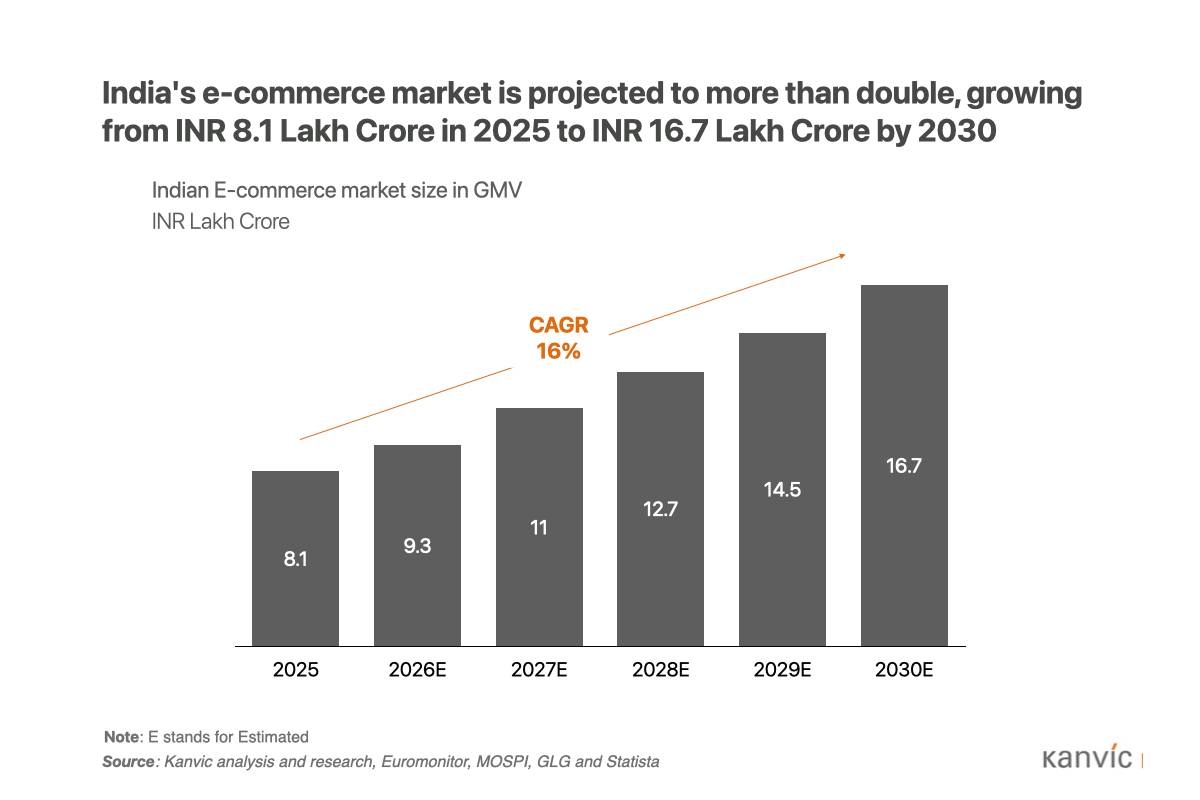

India's e-commerce market crossed ₹8.1 lakh crore in gross merchandise value (GMV) in 2025. Yet online penetration sits at just 10.4% of total retail, against 36.7% in China and 18.1% in the United States. For India Inc., that gap is not a shortfall. It is a runway. The market is set to double to ₹16.7 lakh crore by 2030 at a CAGR of 16%, and the contest to 2030 will not be won on the top line. It will be won by the companies that read the reallocation of channels, categories and consumers early, and build the capabilities to capture the parts of the market they are actually positioned to hold.

This article maps where the growth is going: how large the market becomes, which forces drive it, which segments capture the value, and the strategic questions India Inc. will need to answer to win.

1. The market today: scale with a structural tilt

India's e-commerce market is in a phase of rapid growth and structural transformation. Convenience and deep internet penetration are reshaping purchasing behaviour across the country, reinforced by two enabling shifts: near-universal UPI adoption, which has made digital payment effortless, and mass smartphone access, which has turned every screen into a storefront. On the back of these shifts, the market has reached ₹8.1 lakh crore in GMV by the end of 2025.

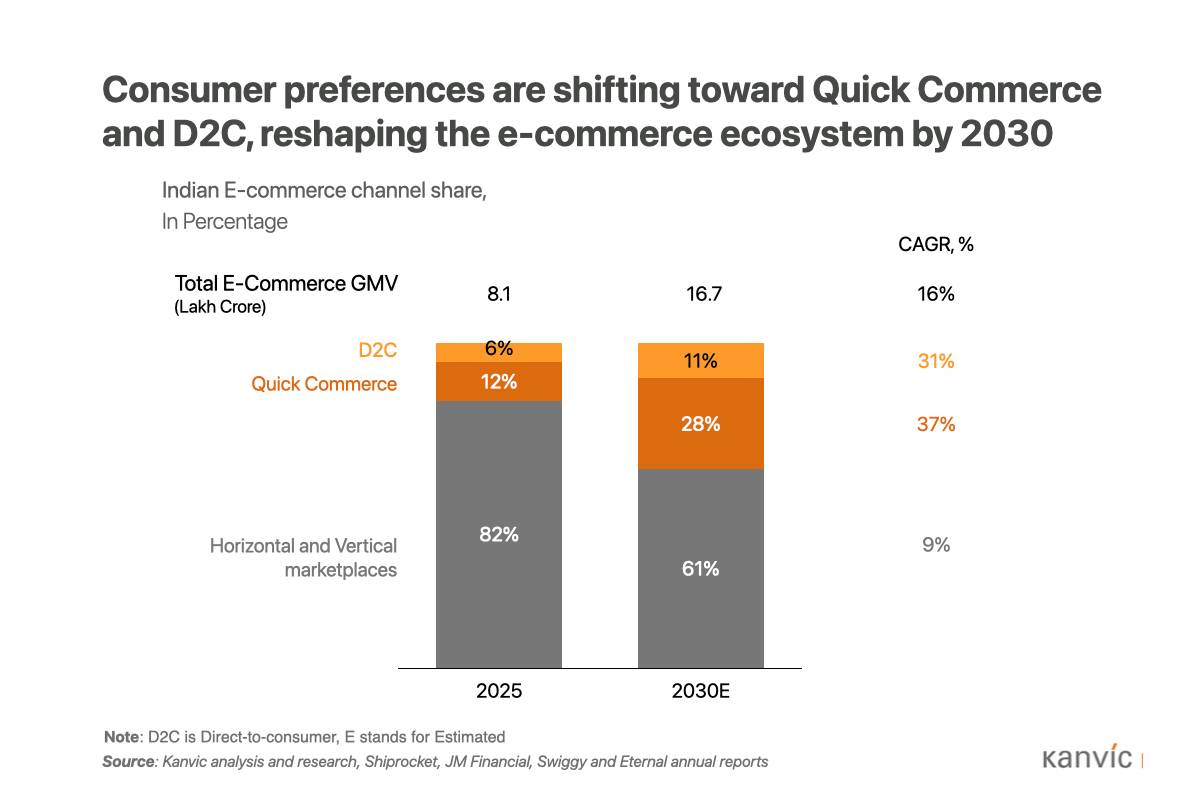

Beneath the headline, the channel split reveals where the momentum already sits. Horizontal and Vertical marketplaces hold 82% of the market. But the alternative formats are expanding fastest: quick commerce has taken 12% of total GMV and brand-owned direct-to-consumer (D2C) platforms account for 6% in 2025.

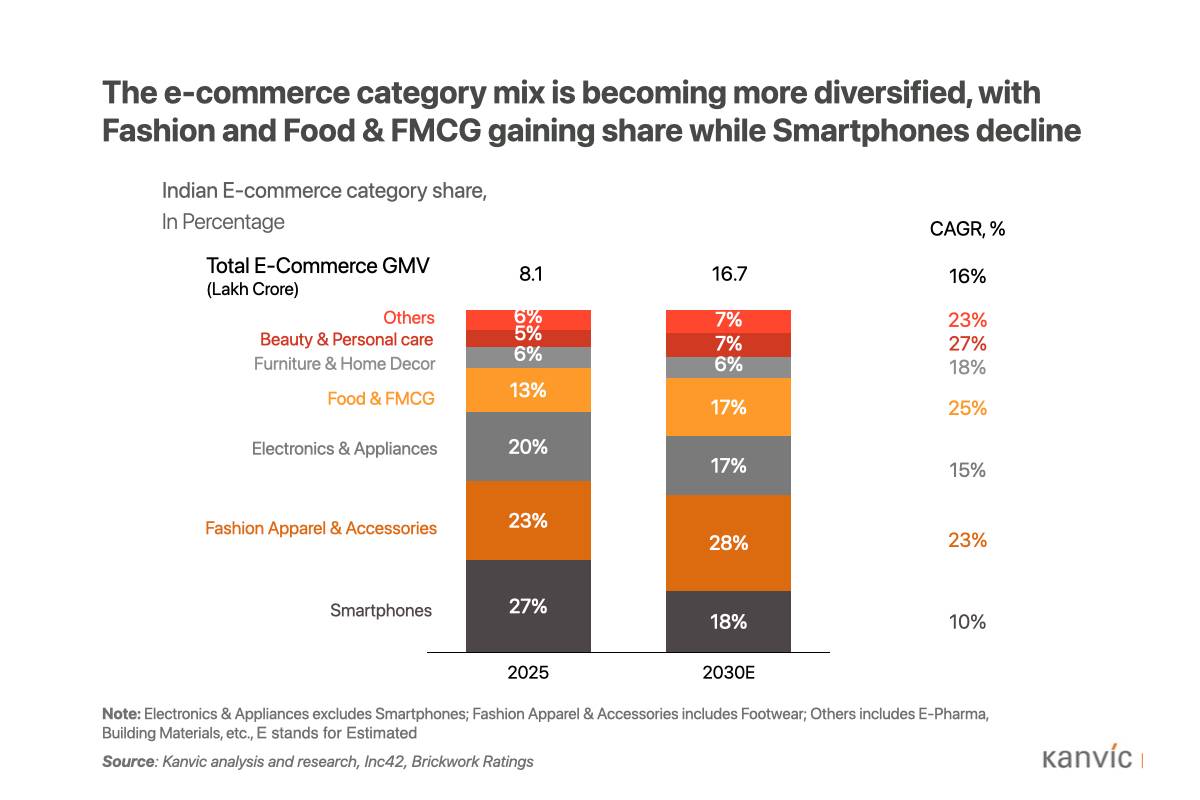

The category mix tells a parallel story. Smartphones command 27% of online GMV and the broader electronics and appliances segment a further 20%, the legacy of an e-commerce era built on high-ticket, low-frequency purchases. Online fashion holds 23%. High-frequency essentials are still under-indexed: food and FMCG at 13%, beauty and personal care at 5%. Furniture and home décor sit at 6% with emerging categories like e-pharmacy, building materials and others, accounting for the remaining 6% in 2025.

2. The growth runway: three drivers shaping the market to 2030

Three drivers will help India’s e-commerce market grow from ₹8.1 lakh crore today to ₹16.7 lakh crore by 2030.

First, Internet penetration is forecast to climb from 65% in 2025 to nearly 85% by the end of the decade, positioning online shoppers to make up 55% of active internet users by 2030. Access is anchored by smartphone ownership in 85.5% of households nationally with at-least 1 smart phone in 2025 rising to 91.3% in urban areas and near-universal among the young.

Second, UPI now processes well over 20 billion transactions a month, functioning as a high-velocity micro-transaction economy in which digital payment displaces cash even for the smallest everyday purchase.

Third, backed by ultra-low data costs and coverage across roughly 20,000 pin codes, leading marketplaces now offer over 100 million SKUs with same-day fulfilment, live tracking and friction-free returns that routinely outperform conventional retail.

3. The blueprint to 2030: channels, categories, consumers

The doubling of the market conceals a more consequential shift: a reallocation of where the value sits. Three movements will define the e-commerce map of 2030.

Channels: commerce becomes quick

The channel mix will be redrawn by 2030, changing both how consumers shop and how brands allocate resources.

- Horizontal and Vertical marketplaces shrink from 82% of total e-commerce GMV in 2025 to around 61% by 2030, as quick commerce pulls away fast-moving food and grocery demand and creeps into other categories in larger towns.

- Quick commerce is on track to command 28% of the market by 2030, up from 12% in 2025. What began as an experimental infrastructure for hyperlocal grocery has become an everyday urban habit.

- D2C platforms are proving durability, not novelty but climbing from 6% in 2025 to 11% by 2030. Driven by the desire for data ownership and margin protection, brands are bypassing intermediaries to secure first-party data, defend premium positioning and build direct loyalty.

Categories: shift to lifestyle and essentials

The first wave of digital retail ran on high-ticket electronics. That playbook is maturing. Momentum is migrating decisively toward lifestyle and high-frequency essentials.

- Fashion leads. Online fashion climbs from 23% in 2025 to 28% by 2030, reaching an estimated ₹4.68 lakh crore in GMV, the single most powerful driver of the market. Growth is fuelled by deeper penetration into Tier-2 and Tier-3 cities, a pivot toward branded apparel, and the rise of agile, ultra-fast lifestyle supply chains.

- Smartphones and electronics stabilise. Smartphones contract from 27% in 2025 to 18% (₹~3 lakh crore) in 2030; electronics and appliances ease from 20% in 2025 to 17% (₹~2.8 lakh crore) in 2030. Their combined online penetration hit a structural ceiling near 47% in 2025. These remain massive in absolute volume, but shift from primary growth engines into mature cash cows built on replacement and premiumisation.

- Daily essentials accelerate. Food and FMCG rise from 13% in 2025 to 17% (₹~2.8 lakh crore) in 2030, drawing level with core electronics by 2030. Beauty and personal care expand from 5% in 2025 to 7% (₹~1.2 lakh crore) in 2030, as online grocery and daily beauty regimens embed into household routines.

- Long-tail categories digitise. Furniture and home décor hold steady at 6% (₹~1 lakh crore) in 2030 as platforms master bulky logistics and larger order values. E-pharmacy, building materials and others inch from 6% in 2025 to 7% (₹~1.2 lakh crore) in 2030, reflecting the steady consolidation of fragmented traditional supply chains into organised digital platforms.

Consumers: the boom in Bharat

The consumer base has moved decisively from a metro-led model toward "Bharat". Tier-2 and Tier-3 cities now drive the bulk of incremental growth. During the 2025 festive sales, roughly 60-65% of online shoppers came from Tier-2 cities, while Tier-3 towns posted around 21% year-on-year order growth and contributed close to 38% of order volumes.

Smaller-city consumers, once seen as conservative, are now more experimental and value-driven, shopping across more categories and expecting faster delivery. The change is driven less by rising incomes than by wider exposure to digital platforms, social commerce and creator ecosystems. Gen Z and middle-income households are the other engines of expansion, with Tier-2-plus cities contributing about half of new e-retail orders in 2025.

4. What this means for India Inc.

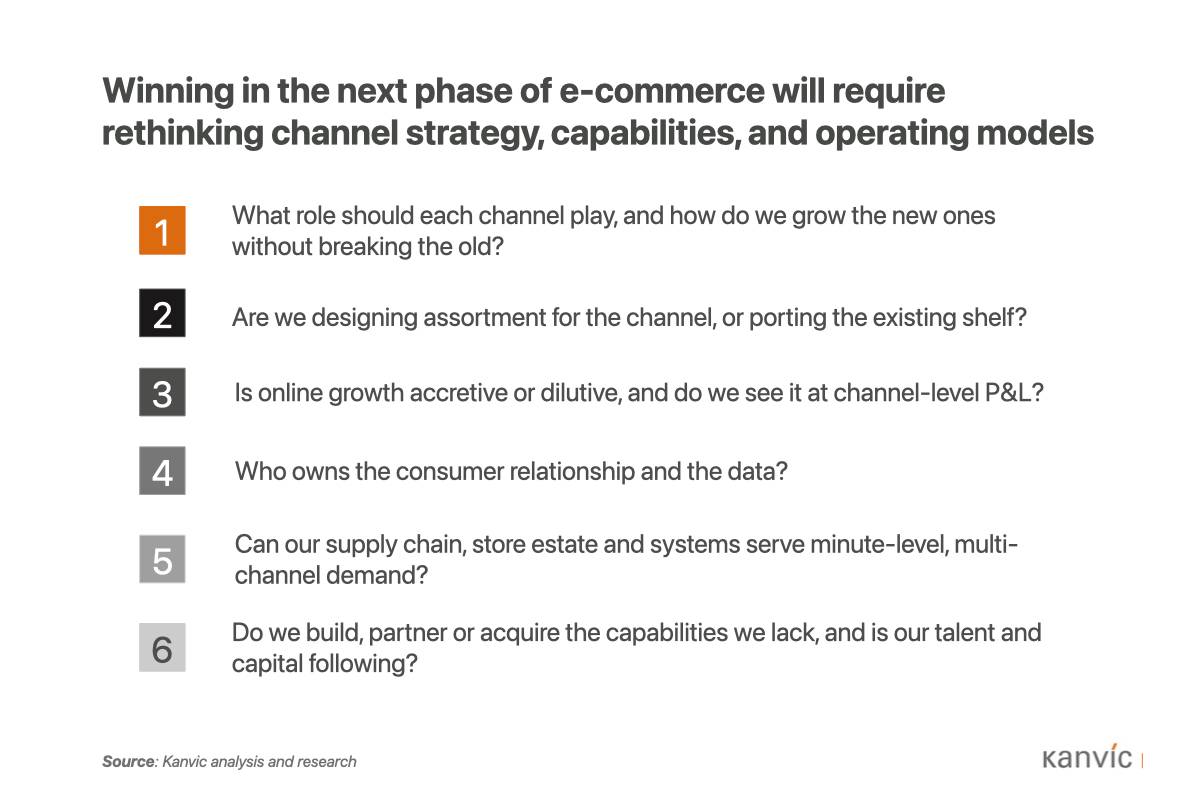

This trajectory hands established players an unusual advantage. FMCG, consumer durables, retail and building-materials companies already command the brands, balance sheets and distribution muscle that digital-native challengers spend years and enormous capital trying to build. The opportunity is theirs to shape, but only if they engage six strategic questions while they still have the strength to determine the outcome.

1. What role should each channel play, and how do we grow the new ones without breaking the old?

Quick commerce is becoming the dominant online channel, not a sub-segment of it; in FMCG, the majority of e-commerce volume already flows through it. India Inc. will need to assign each channel a deliberate role and ceiling, then design go-to-market so quick commerce and D2C scale without cannibalising the general-trade and distributor economics that remain the incumbent's defensible advantage.

2. Are we designing assortment for the channel, or porting the existing shelf?

Winning ranges are channel-specific, not the physical shelf listed online. In FMCG, that means premium, margin-rich packs and adjacency formats built for quick commerce, while low-unit-price mass packs stay in general trade; in durables and building materials, the online-relevant SKU set diverges from the trade range. The question is whether SKUs, pack architecture, price points and launches are built for how people actually buy in each channel.

3. Is online growth accretive or dilutive, and do we see it at channel-level P&L?

The same "strong online growth" headline hides opposite economics. Marketplace commissions, advertising spend and returns can compress net margins to low single digits, while a premiumised quick-commerce mix can be gross-margin accretive. Without a true channel-by-channel P&L, top-line growth can quietly mask margin erosion, making this a resource-allocation question, not a commercial one.

4. Who owns the consumer relationship and the data?

Marketplaces and quick commerce return little to no consumer data, leaving brands blind to who buys, how often and why they lapse. For businesses that historically sold through intermediaries, the decision is how much to invest in owned channels and first-party data for the innovation, retention and pricing power it buys, versus simply renting reach.

5. Can our supply chain, store estate and systems serve minute-level, multi-channel demand?

Service has shifted from days to minutes, and from a handful of channels to eight or more running at once. This tests whether the physical network, including stores repurposed as fulfilment nodes and the technology spine, such as a single inventory pool, deep integrations, a reliable system of record, are built for granular, real-time operations. It is most consequential in durables and building materials, where last-mile logistics and installation are genuine differentiators rather than cost lines.

6. Do we build, partner or acquire the capabilities we lack, and is our talent and capital following?

Few incumbents can build data, digital-marketing and fulfilment-technology capability organically at the required pace. The question is where each capability is a real source of advantage worth owning versus a commodity best rented, and whether leadership talent and capital are being reallocated toward where the market is heading, rather than treating digital as an under-funded adjacency.

The window, and the choice

The size of the e-commerce opportunity is well established: over ₹16.7 lakh crore by 2030, with the value migrating from marketplaces to quick commerce and D2C, and from electronics to fashion and daily essentials. The strategic question is narrower and more urgent, which part of that market your company is positioned to capture, and whether you are building the capability to do so before the window narrows.

Companies that engage these questions now, while they still hold the balance-sheet and brand strength to shape the outcome, will define the next phase of Indian consumption rather than adjust to it.

Related Insights