AI is now moving from aspiration to application. As one media and entertainment leader put it, “now with Generative AI, we finally have found a very effective tool.”

In the cement and building materials sector, companies are deploying AI-enabled central control systems to optimise network operations.

In logistics businesses, “agentic AI” is being used to automate documentation and enhance operational efficiency. In retail, AI initiatives are now among the top three keywords, alongside market growth and consumer confidence.

India Inc.’s leadership no longer considers AI readiness as optional. Our CEO Agenda Q2 2025 tracked how this shift began earlier in the year. Companies that delay investment in AI capabilities—whether in demand forecasting, supply chain optimisation, or customer engagement—risk falling behind competitors who are already realising tangible efficiency gains.

Tariffs, Trade Deals and Supply Chains: The New Strategic Calculus

Trade policy and geopolitical risk have become permanent features of the CEO agenda. While trade policy mentions remain steady (+1% QoQ), the underlying conversation has become more nuanced and sector-specific.

In textiles and apparel, tariff impacts and trade agreements are the top keywords, reflecting the sector’s acute sensitivity to shifts in global trade flows. In automotive and industrial products, supply chain challenges and import restrictions are driving a reassessment of sourcing and localisation strategies.

The European market, in particular, presents a genuinely mixed picture. On one hand, softening European consumer demand and weak macroeconomic conditions are creating headwinds for Indian companies with significant B2C or automotive export exposure. On the other hand, the contraction of European industrial capacity in sectors like specialty chemicals and pharmaceuticals is creating supply gaps that Indian companies are actively moving to fill.

As one chemicals company observed, while European competitors are retreating or reducing capacity, Indian firms see a window to capture market share and strengthen customer relationships. Separately, the phased implementation of India-EU trade agreements is opening new export pathways in textiles, specialty products, and building materials, with one management team describing the impact as creating “immediate and ongoing opportunities to increase exports and margins.”

The bottomline is that geopolitical risk demands continuous scenario planning, agile supply chain management, and proactive engagement with trade policy developments. Companies that build these capabilities into their strategic planning process will navigate uncertainty far more effectively than those that react after the fact.

Premiumisation as Margin Defence: A Cross-Sector Playbook

Consumer behaviour mentions remain robust (+2% QoQ), but the more telling signal lies in that premiumisation trend has emerged as a consistent theme across sectors. From FMCG and paints to cement and consumer durables, India Inc.’s leaders are betting on premium products as the primary lever for margin expansion and brand differentiation.

In building materials, the shift toward higher-performance, value-added products, aided by regulatory changes and evolving consumer preferences, is creating new pricing power.

In FMCG, the rapid growth of quick commerce and digital channels is accelerating the premiumisation trend, as these platforms disproportionately attract higher-value consumers.

In the decorative paints segment, the drive toward premium offerings is being deployed as a defence against intensifying price competition from new entrants.

In the electrical goods space, management teams report that the focus on premium products, particularly energy-efficient offerings, is “driving revenue growth and margin resilience.”

Leading companies understand that the key to success lies in understanding that premiumisation is about delivering measurably superior value, not simply about charging more . Companies that invest in product innovation, channel-specific strategies, and brand elevation capture the margin benefits; those that pursue premiumisation without a genuine value proposition risk alienating consumers in an increasingly discerning market.

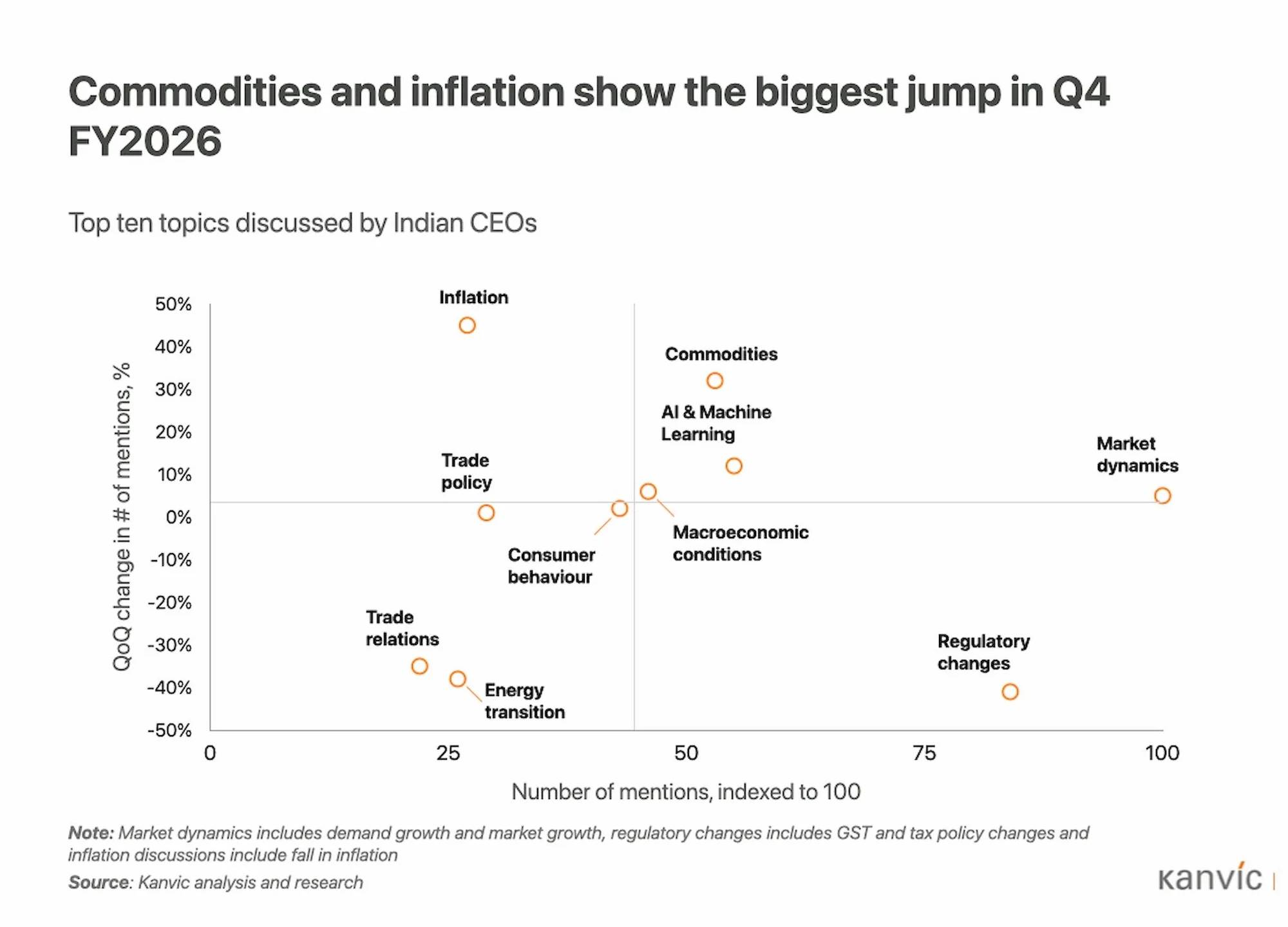

Inflation: Return to the Conversation

Perhaps the most notable signal in our quantitative analysis is the 45% quarter-on-quarter jump in inflation-related mentions, the sharpest rise of any theme on the CEO agenda. While inflation had receded from peak levels in earlier quarters, its return to the boardroom conversation suggests that cost pressures are far from resolved. Moreover, the increasing risk to the energy infrastructure in the Middle East point towards more pain in the coming quarters.